البحث في الموقع

عرض النتائج للدليل 'auditing'.

-

معايير المراجعة الدولية الترجمة المعتمدة بالإضافة إلى كتاب معايير المراجعة international auditing and assurance standards handbook 20082008_IAASB_Handbook_Part_I-Compilation.pdf 2008_IAASB_Handbook_Part_II-Compilation.pdf Audit Book 2008 P1 .pdf Audit Book 2008 P2.pdf

معايير المراجعة الدولية الترجمة المعتمدة بالإضافة إلى كتاب معايير المراجعة international auditing and assurance standards handbook 20082008_IAASB_Handbook_Part_I-Compilation.pdf 2008_IAASB_Handbook_Part_II-Compilation.pdf Audit Book 2008 P1 .pdf Audit Book 2008 P2.pdf -

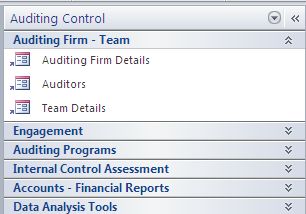

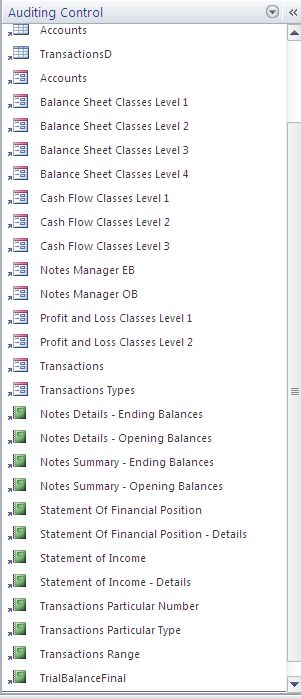

السادة الزملاء الأعزاء مدققي الحسابات على مستوى الوطن العربي أتشرف بأن أقدم لكم لمحة بسيطة في السطور القادمة حول برنامج إدارة مهام التدقيق الجديد AuditingControl الإصدار 1.61 هل حلمت كمدقق حسابات ببرنامج بسيط يتيح لك أدوات تدقيق متقدمة ؟ هل تريد أن تسيطر بشكل كامل على مهام التدقيق ؟ هل تريد كمدير تدقيق أن تدير فريقك بفاعلية كبيرة مع قياس للإداء يمكنك بأن تحسن مستوى خدمات التدقيق لديك هل تريد برنامج مجاني للقيام بذلك كله ؟ نعم كل ذلك و أكثر متوفر في برنامج إدارة مهام التدقيق الجديد AuditingControl الإصدار 1.61 برنامج إدارة مهام التدقيق AuditingControl هو أحد الحلول المصممة بواسطة قواعد بيانات Access و التي تتيح للمدقق العديد من الأدوات التي تساعد على أداء مهام التدقيق بفاعلية شديدة و مدة تطوير هذا الحل من بداية شهر نوفمبر 2009 و حتى الآن و لقد وضعناه تحت التجربة بشكل مكثف للتأكد من الوصول بأداء عالي لهذا الحل المهم برنامج إدارة مهام التدقيق يرتكز على فكرة أنه لكل شركة و لكل سنة مالية محل التدقيق قاعدة بيانات منفصلة و هذه هي الشاشات الرئيسية التي توضح القوائم التي بها جميع النماذج و التقارير الصورة السابق توضح الشاشة الرئيسية توضح القائمة الرئيسية على الجانب الأيسر و هي تتكون من ستة قوائم رئيسية هي القائمة الأولى : معلومات شركة التدقيق و مجموعات التدقيق القائمة الثانية : معلومات مهمة التدقيق القائمة الثالثة : البرامج الإجرائية للتدقيق القائمة الرابعة : تقييم نظم الرقابة الداخلية القائمة الخامسة : الحسابات و القوائم المالية القائمة السادسة : أدوات تحليل البيانات برنامج إدارة مهام التدقيق AuditingControl سوف يكون مجاناً تماماً لمن سيشتركون في دورة التدريب الخاصة بالبرنامج و هذه الدورة سوف تكون بسعر مناسب بحيث يمكن لأي مدقق بشكل شخصي أو من خلال المكتب الذي يعمل لديه أن يشترك و هذه الدورات سوف تكون عبارة عن دروس فيديو مصورة توضح كيفية أستخدام هذا البرنامج بشكل كفؤ الأمكانيات الخاصة ببرنامج إدارة مهام التدقيق AuditingControl الإصدار 1.61 هي كالتالي أمكانية إدخال معلومات فريق التدقيق و تقسيم العمل و إدارته Auditing Team أمكانية إرفاق الملفات بشكل ألكتروني في العديد من نوافذ البرنامج و هذه المرفقات من الممكن أن تكون ملفات أكسيل أو وورد أو بي دي أف أو صور Attachments أمكانية إدارة المرفقات الخاصة بقضايا الخبرة القضائية Forensic Auditing Attachments Management أمكانية تخطيط عملية التدقيق Auditing Planning أمكانية وضع خطوات البرامج الإجرائية للتدقيق Auditing Procedures وجود برامج إجرائية جاهزة لعمليات التدقيق يمكن تطبيقها بشكل مباشر Auditing Programs أمكانية كتابة ملاحظات عمليات التدقيق و طباعة تقارير خطوات البرامج الإجرائية لعمليات التدقيق أمكانية تنظيم أوراق العمل ألكترونياً لجميع عمليات التدقيق Working Papers Management أمكانية وضع أستقصاءات الرقابة الداخلية Internal Control Questionnaire تحديد نتيجة استقصاءات الرقابة الداخلية بنظام القوائم المرجحة بأوزان الأهمية النسبية أو ما يعرف Quantified Internal Control Questionnaire أمكانية تحديد مواطن الضعف الخاصة بنظم الرقابة الداخلية من خلال التقارير Internal Control Weak Points أمكانية إستيراد الحسابات و أكوادها أمكانية تصنيف الحسابات مع وجود تصنيفات تتوافق مع المبادئ المحاسبية المتعارف عليها GAAP أمكانية إدخال قيود التسوية و تتبعها بشكل دقيق Adjustments Transactions أمكانية إدخال ملاحظات التدقيق و تتبعها بشكل دقيق Auditing Notes أمكانية الحصول على تقرير ميزان المراجعة Trial Balance أمكانية الحصول على قائمة الدخل Income Statement أمكانية الحصول على قائمة المركز المالي Statement of Financial Position أمكانية تحليل البيانات بأستخدام قانون بنفورد Benford's Law مثل تحليل أول رقم و تحليل ثاني رقم و تحليل ثالث رقم و تحليل أول رقمين و تحليل أول ثلاث أرقام و تحليل أول رقمين من الموضع الثاني ( تحليل جديد لا يوجد في أي تطبيق ) وجود نظام للنسب المالية Ratio Analysis أمكانية أستخراج تقارير تقادم الديون Aging Reports أمكانية أستخراج القيم المكررة في البيانات Dublicates Find أمكانية أستخراج تقارير التقسيمات الطبقية للبيانات Stratification of Data أمكانية مقارنة مجموعتين من البيانات Two Set Comparison تقرير ملخص جانبي للبيانات Data Profile برنامج إدارة مهام التدقيق AuditingControl ينافس و بشدة البرامج الشهيرة مثل CaseWare و ACL و في ميدان العمل أثبت البرنامج جدارته بشكل كبير و لاحظنا أن عملاء التدقيق لدينا قد لاحظوا مدى قوة مخرجات البرنامج و ذلك من خلال نظام إدارة التسويات و المرفقات و التقارير المالية المستخرجة للمعلومات و الأستفسار يمكن زيارة ملفي الشخصي و به كل معلومات الأتصال من ( هنا ) بالتوفيق

-

انقر: http://www.ifac.org/Guidance/ http://www.iasplus.com/ifac/iaasb.htm

انقر: http://www.ifac.org/Guidance/ http://www.iasplus.com/ifac/iaasb.htm -

هنا بإذن الله تعالى سندرج التراجم و المناقشات الخاصة بموضوع المراجعة الداخلية أو Internal Auditing

-

أود ان اعرض عليكم اليوم شهادة من الشهادات الهامة فى مصر وهى ليست بشهادة مهنية ولكنها تعدك للدخول الى شهادة من الشهادات المهنية مثل cma,acca . لأن اغلب المواد بها تقريبا موجودة بالمواد التى تدرس فى مناهج الشهادات المهنية. وهذة الشهادة هى التى قمت بدراستها والحمد لله انهيتها بتقدير جيد جدا وافادتنى كثيرا... حيث اقوم الان بتحضير Acca ويقوم بتدريس مواد هذة الشهادة نخبة من أكبر الاساتذة الحاصلين على أعلى الشهادات المهنية , وأقدم اليكم نبذة عن هذة الشهادة وانصح بها جميع الخريجين والطلاب الدارسين فى كليات التجارة: وهذة المعلومات من موقع الجامعة الامريكية بالقاهرة وهذا الرابط الخاص بالموضوع على موقع الجامعة الامريكية: http://www.aucegypt.edu/conted/sce/bus-profaccandfin.html وبالمرفقات ملخص للشهادات المقدمة من الجامعة الامريكية من مركز التعليم المستمر وشرح أكثر لهذة الشهادة. Professional Certificate in Accounting & Financing A graduate certificate designed to provide participants with the combination of accounting and financial management expertise. Certificate graduates are prepared to meet the demand for professionals in financial accounting and internal auditing, management accounting, and financial management. The certificate curriculum qualifies the graduates to sit for the exams of the CMA program as well as the first and second level of ACCA exams. Admission Requirements: University graduate or holds the ‘Certificate in Accounting and Finance’ English Proficiency Test (EPT): 71% minimum or General English Level 302 Interviews: Vocational Tendency (VT) and English Oral Placement Test (EOPT) Courses: The certificate consists of the following fourteen, 3-IU courses: وهذة المواد الخاصة بالدراسة. Preparation of Financial Statements Business Economics Financial Management and Control Managing People Financial Reporting Accounting Information System Management Accounting I Financial Analysis Corporate Reporting Management Accounting II Auditing, Internal Review Direct Tax General Sales Tax Banking Operations Graduation Requirements: Complete all certificate courses GPA: 2.5 minimum Details on courses can be viewed or printed by clicking on the Course and Certificate Catalog cace-catalog.pdf

أود ان اعرض عليكم اليوم شهادة من الشهادات الهامة فى مصر وهى ليست بشهادة مهنية ولكنها تعدك للدخول الى شهادة من الشهادات المهنية مثل cma,acca . لأن اغلب المواد بها تقريبا موجودة بالمواد التى تدرس فى مناهج الشهادات المهنية. وهذة الشهادة هى التى قمت بدراستها والحمد لله انهيتها بتقدير جيد جدا وافادتنى كثيرا... حيث اقوم الان بتحضير Acca ويقوم بتدريس مواد هذة الشهادة نخبة من أكبر الاساتذة الحاصلين على أعلى الشهادات المهنية , وأقدم اليكم نبذة عن هذة الشهادة وانصح بها جميع الخريجين والطلاب الدارسين فى كليات التجارة: وهذة المعلومات من موقع الجامعة الامريكية بالقاهرة وهذا الرابط الخاص بالموضوع على موقع الجامعة الامريكية: http://www.aucegypt.edu/conted/sce/bus-profaccandfin.html وبالمرفقات ملخص للشهادات المقدمة من الجامعة الامريكية من مركز التعليم المستمر وشرح أكثر لهذة الشهادة. Professional Certificate in Accounting & Financing A graduate certificate designed to provide participants with the combination of accounting and financial management expertise. Certificate graduates are prepared to meet the demand for professionals in financial accounting and internal auditing, management accounting, and financial management. The certificate curriculum qualifies the graduates to sit for the exams of the CMA program as well as the first and second level of ACCA exams. Admission Requirements: University graduate or holds the ‘Certificate in Accounting and Finance’ English Proficiency Test (EPT): 71% minimum or General English Level 302 Interviews: Vocational Tendency (VT) and English Oral Placement Test (EOPT) Courses: The certificate consists of the following fourteen, 3-IU courses: وهذة المواد الخاصة بالدراسة. Preparation of Financial Statements Business Economics Financial Management and Control Managing People Financial Reporting Accounting Information System Management Accounting I Financial Analysis Corporate Reporting Management Accounting II Auditing, Internal Review Direct Tax General Sales Tax Banking Operations Graduation Requirements: Complete all certificate courses GPA: 2.5 minimum Details on courses can be viewed or printed by clicking on the Course and Certificate Catalog cace-catalog.pdf -

good day DR.alsawalha my name is noura , i'm an auditing master students, actually dr, i'd like to write a thesis about merger and acquisition and the auditor role in, i mean evaluation the assets , or the kind of evidence does auditor gater in case of merger , but my problem i don't know to start from where please i need your help there ; is it a good thesis , is it possible to make please me by giving me some hints i'm looking forward for your great aid and thank alots

-

good day DR.alqashi my name is noura , i'm an auditing master students, actually dr, i'd like to write a thesis about merger and acquisition and the auditor role in, i mean evaluation the assets , or the kind of evidence does auditor gater in case of merger , but my problem i don't know to start from where please i need your help there ; is it a good thesis , is it possible to make please me by giving me some hints i'm looking forward for your great aid and thank alots

good day DR.alqashi my name is noura , i'm an auditing master students, actually dr, i'd like to write a thesis about merger and acquisition and the auditor role in, i mean evaluation the assets , or the kind of evidence does auditor gater in case of merger , but my problem i don't know to start from where please i need your help there ; is it a good thesis , is it possible to make please me by giving me some hints i'm looking forward for your great aid and thank alots -

good day DR.TAWFIK my name is noura , i'm an auditing master students, actually dr, i'd like to write a thesis about merger and acquisition and the auditor role in, i mean evaluation the assets , or the kind of evidence does auditor gater in case of merger , but my problem i don't know to start from where please i need your help there ; is it a good thesis , is it possible to make please me by giving me some hints i'm looking forward for your great aid and thank alots

-

السلام عليكم ورحمة الله وبركاته أرجو بيان صحة الترجمة لما يلي: (حسابات العملاء، الموردون، محاسبة الرواتب والأجور، تدقيق المصروفات وتصفيتها، إعداد عروض الأسعار،متابعة الجانب المالي لعقود الشركة، إعداد القوائم المالية الختامية، إعداد الموازنة التقديرية، إعداد الدراسات المالية : نقطة التعادل، قائمة التدفق النقدي) (Accounts of customers, suppliers, salaries accounting, auditing and liquidation expenses, the preparation of quotations, follow-up of the financial aspect of the company's contracts, the preparation of the final financial statements, preparation of budget estimates, preparation of financial studies: Break-even analysis, Cash flow statement) كما أرجو ترجمة (الرقابة الشرعية على منتجات الشركة) جزاكم الله خيرا وجعل ذلك في ميزان حسناتكم

-

برجاء المساعدة باحدث المقالات و المؤتمرات الخاصة بوضوع strategic systems auditing او ما يسمى business risk audit خاصه كتاب - Lemon, M., K. W. Tatum., and W. S. Turley (2000). Developments in the Audit Methodologies of Large Accounting Firms. Hertford, UK: Steephen Austuin & Sons, Ltd, وجزيل الشكر على اهتمامكم .

-

Acronyms & Abbreviations ABL Accepted batch listing ALTA American land title association ATRR Allocated transfer risk reseve BAN Bond anticipation note bp Basis point CAMELS Capital, asset quality, management, earning, liquidity, sensitivity CAPM Capital asset pricing model CBCT Customer-bank communication terminal CHAPS Clearing house automated payments system COM Computer output microfilm CUNA Credit union national association DDA Demand deposit accounting DDA Demand deposit account DDA Direct deposit account DSO Days sales outstanding EBT Electronic benefit transfer ECU European currency unit FAS Financial accounting standards FASB Financial accounting standards board FINS Financial industry numbering standard GAAB Generally accepted accounting principles GAAS Generally accepted auditing standards HDGS High dollar group sort IRR Iternal rate of return I/S Inventory to sales ratio LEAPS Long-term equity anticipation securities MBO Management by objective NOI Net operating income OECD Organization for economic coorperation and development P/E Price earnings ratio ROA Return on assets ROE Return on equity ROI Return on investment

Acronyms & Abbreviations ABL Accepted batch listing ALTA American land title association ATRR Allocated transfer risk reseve BAN Bond anticipation note bp Basis point CAMELS Capital, asset quality, management, earning, liquidity, sensitivity CAPM Capital asset pricing model CBCT Customer-bank communication terminal CHAPS Clearing house automated payments system COM Computer output microfilm CUNA Credit union national association DDA Demand deposit accounting DDA Demand deposit account DDA Direct deposit account DSO Days sales outstanding EBT Electronic benefit transfer ECU European currency unit FAS Financial accounting standards FASB Financial accounting standards board FINS Financial industry numbering standard GAAB Generally accepted accounting principles GAAS Generally accepted auditing standards HDGS High dollar group sort IRR Iternal rate of return I/S Inventory to sales ratio LEAPS Long-term equity anticipation securities MBO Management by objective NOI Net operating income OECD Organization for economic coorperation and development P/E Price earnings ratio ROA Return on assets ROE Return on equity ROI Return on investment -

بالاطلاع علي تجارب الدول العربية في بناء معاييرها للمحاسبة نجد ان معظمها يتميز بخصائص: البعد عن اصدار معايير اسلامية للمحاسبة – عدم وجود تنظيم متكامل لاصدارها ومتابعتها بكل جديد – عدم وجود موقع مستقل علي الانترنت لمتابعتها وغير ذلك. وعلي خلاف ذلك لاحظ الباحث تميز التجربة الماليزية وشمولها لاهم المعايير الاسلامية. كذلك تصدر هيئة المحاسبة والمراجعة للمؤسسات المالية الاسلامية AAOIFI بالبحرين معايير محاسبية طبقا للشريعة الاسلامية لم يتم الاستفادة منها بعد بالكامل. وقد دفعت تلك الاعتبارات الباحث لبحث موضوع بيان سبل استكمال بناء تلك المعايير الوطنية والعربية. وقد تناول البحث هذه الاعتبارات من خلال قسمين: الاول شمل دراسة مقارنة لخصائص بناء المعايير في الدول والهيئات الوطنية والعربية، وعرض وتقييم التجارب المصرية والماليزية والسعودية ومجلس التعاون الخليجي في بناء معايير المحاسبة المالية. اما القسم الثاني فشمل اطارا مقترحا لبناء المعايير الاسلامية لمحاسبة الزكاة السعودي وعرض القوائم المالية في المؤسسات المالية الاسلامية من المعيار الماليزي. وقد انتهي البحث الي بيان مدي شمول وجودة التجربة الماليرية واوجة قصور واستكمال التجارب العربية في بناء المعايير المحاسبية من خلال: ضرورة استكمال محورها التنظيمي وانشاء مجالس معايير المحاسبة ومواقعها علي الانترنت وبناء معاييرها الاسلامية ودعمها بكل جديد. ويتعين قي هذا الشأن الاسترشاد بتجربة الـ 21 معيار اسلامي Shari’a Standards (SSs) التي اصدرتها هيئة المحاسبة والمراجعة للمؤسسات المالية الاسلامية Accounting and Auditing Organization for Islamic Financial Institutions عام 2005 بمملكة البحرين. انقر: http://mstawfik.tripod.com/is.pdf

-

اصدر السيد الأستاذ الدكتور محمود محي الدين اليوم قرارا وزاريا رقم 243 لعام 2006 بشأن إصدار معايير المحاسبة المصرية الجديدة والتي تحل محل معايير المحاسبة الجاري تطبيقها حاليا والتي سبق إصدارها بالقرارين الوزاريين رقمي 503 لسنة 1997، 345 لسنة 2002. ويبلغ عدد معايير المحاسبة التي صدر بشأنها القرار الوزاري عدد 35 معيارا تتضمن عدة معايير لم تكن قد صدرت بعد لتكتمل منظومة معايير المحاسبة المصرية لتصبح متفقة تماما مع معايير المحاسبة الدولية. وجدير بالذكر أن المعايير الجديدة للمحاسبة تم إصدارها لتتماشى مع التغيرات الإقتصادية والتقدم العلمى والتقنى سواء على مستوى أداء الأعمال فى الشركات أو على مستوى النظم المحاسبية فيها. ومن المؤكد أن وجود معايير محاسبة مصرية متوافقة مع المعايير الدولية وملزمة لجميع الشركات سوف يؤدي بالضرورة إلى ارتفاع جودة القوائم المالية بما فيها من إفصاح وشفافية تساعد جميع المهتمين بهذه الشركات في فهم هذه القوائم و إتخاذ قراراتهم الاقتصادية والمالية على أساس سليم يتمثل فى قوائم مالية أعدت طبقاً لأحدث ما صدر فى العالم من معايير وتوضح الأوضاع المالية الفعلية لتلك الشركات. كما يعتبر إصدار هذه المعايير اليوم خطوة هامة وأساسية تساهم في تحسين تطبيق الشركات لمبادئ ومعايير حوكمة الشركات. New accounting standards boost transparency Disclosure and transparency will be supported by new accounting standards. Companies will have better financial statements that investors, donors and regulators will be able to analyse more easily, The new Egyptian accounting standards were approved when the Minister of Investment, Dr. Mahmoud Mohieldin issued Decree # 243/2006. The new standards are in compliance with international standards and will help international investors to consider companies in Egypt for investment. In turn, corporate governance principles will be boosted, companies' efficiency will increase and the cap l market and economy will perform better. The decree was issued after the 3rd meeting of the committee including members of the Cap l Market Authority, the Egyptian Accountants and Auditors Association (EAAA) and the Central Auditing Organisation. The new standards include 39 new rules. The old standards have been in effect for 10 years and require upgrading. Accountants and auditors can now refer to the Egyptian version of the standards. The meeting was attended by the chairman of the Egyptian Accountants and Auditors Institute and the former prime minister, Dr. Abdel Aziz Hegazi; CMA chairman, Dr. Hani Seri; EAAA chairman, Mr. Hazem Hasan; chairman of accounting practitioners section, Mr. Hafez Mostafa; senior advisor to the minister, Mr. Abdel Hamid Ibrahim; advisor to the minister, Dr. Atef Al Nokali; advisor to the chairman of EAAA and Mr. Mohammed Hasib, representative of the General Authority for Investment and Free Zones.

-

For all Internal Auditor the IIA CD "Internal Auditing Manual Shell". The objective of this CD is to assist internal auditing dept. in developing or enhancing an internal auditing manual shell.rar

For all Internal Auditor the IIA CD "Internal Auditing Manual Shell". The objective of this CD is to assist internal auditing dept. in developing or enhancing an internal auditing manual shell.rar -

بالاطلاع علي تجارب الدول العربية في بناء معاييرها للمحاسبة نجد ان معظمها يتميز بخصائص: البعد عن اصدار معايير اسلامية للمحاسبة – عدم وجود تنظيم متكامل لاصدارها ومتابعتها بكل جديد – عدم وجود موقع مستقل علي الانترنت لمتابعتها وغير ذلك. وعلي خلاف ذلك لاحظ الباحث تميز التجربة الماليزية وشمولها لاهم المعايير الاسلامية. كذلك تصدر هيئة المحاسبة والمراجعة للمؤسسات المالية الاسلامية AAOIFI بالبحرين معايير محاسبية طبقا للشريعة الاسلامية لم يتم الاستفادة منها بعد بالكامل. وقد دفعت تلك الاعتبارات الباحث لبحث موضوع بيان سبل استكمال بناء تلك المعايير الوطنية والعربية. وقد تناول البحث هذه الاعتبارات من خلال قسمين: الاول شمل دراسة مقارنة لخصائص بناء المعايير في الدول والهيئات الوطنية والعربية، وعرض وتقييم التجارب المصرية والماليزية والسعودية ومجلس التعاون الخليجي في بناء معايير المحاسبة المالية. اما القسم الثاني فشمل اطارا مقترحا لبناء المعايير الاسلامية لمحاسبة الزكاة السعودي وعرض القوائم المالية في المؤسسات المالية الاسلامية من المعيار الماليزي. وقد انتهي البحث الي بيان مدي شمول وجودة التجربة الماليرية واوجة قصور واستكمال التجارب العربية في بناء المعايير المحاسبية من خلال: ضرورة استكمال محورها التنظيمي وانشاء مجالس معايير المحاسبة ومواقعها علي الانترنت وبناء معاييرها الاسلامية ودعمها بكل جديد. ويتعين قي هذا الشأن الاسترشاد بتجربة الـ 21 معيار اسلامي Shari’a Standards (SSs) التي اصدرتها هيئة المحاسبة والمراجعة للمؤسسات المالية الاسلامية Accounting and Auditing Organization for Islamic Financial Institutions عام 2005 بمملكة البحرين. http://mstawfik.tripod.com/is.pdf

-

This figure shows the close link between auditing and th socio-economic environment it serves in English-spesking world. In particular, it shows: how audit objectives have changed in response to changes in the socio-economic environment. how the main centre of auditing development shifted from the United Kingdom (UK) to the United States of America (USA). how the procedures adopted by auditors accord with the objectives auditing is trying to meet. Also, shows that the development of auditing can be considered conveniently in five phases: period up to 1844, 1920s - 1844 1920s - 1960s 1960s - 1990s 1990s - present.

This figure shows the close link between auditing and th socio-economic environment it serves in English-spesking world. In particular, it shows: how audit objectives have changed in response to changes in the socio-economic environment. how the main centre of auditing development shifted from the United Kingdom (UK) to the United States of America (USA). how the procedures adopted by auditors accord with the objectives auditing is trying to meet. Also, shows that the development of auditing can be considered conveniently in five phases: period up to 1844, 1920s - 1844 1920s - 1960s 1960s - 1990s 1990s - present. -

this is my first participation in this community I hope to be benefit to you, it's about: Is the audit expectation gap a major issue facing the audit profession? Yes, the audit expectation gap is perceived to be one of the major issues facing the audit profession .The users of company reports expect auditors to detect and report material fraud and irregularities amongst other issues. In return, the profession argues that the users misunderstand the duty of auditors, and that fraud detection and reporting is not a central audit objective. Papadakis (2003) says that the auditing profession ignores, at its peril, the debate about its ability to deliver what the market wants, thus the users worldwide expect auditors to detect fraud and actively search for it. For example, If a survey were carried out within the general public and members of the public were asked to give a “true” or “false” answer to the statement : “The role of the auditor is to detect fraud and error in financial statements”, most people would say true. If users of financial statements and the general public were educated to think that the auditor's role embraces the detection and prevention of fraud, especially in relation to material items, the fraud and error detection role of an audit could be relatively objective. However, absolute objectivity cannot be guaranteed since “materiality” and “material significance” are subjective concepts which require furthe clarification by the Auditing Practices Board. A return to the primary role of detection and prevention would also be welcomed since there are at present, not sufficient measures to hold the auditor liable for negative consequences of his actions. Some sources of academic literature assume that the meaning of an audit is not objective/fixed whilst other sources such as contents of audit reports assume that the meaning of an audit is fixed. In relation to the latter assumption, there is the belief that the expectations gap could be significantly reduced – if not possible to eliminate. Is it Possible to Eliminate the Expectations Gap? According to Sikka et al, the nature of the components of the expectations gap make it difficult to eliminate. Perceived performance of auditors is an element which is difficult to measure and changes constantly. It is however possible to substantially reduce but not totally eliminate. The structureof the audit expectation gap is deptcted in the next figure: http://www.infotechaccountants.com/forums/picture.php?albumid=19&pictureid=57 Structure and composition of the audit expectation gap Analysis of the audit expectation-performance gap reveals that it has two major components (porter 1991, 1993 first, The reasonableness gap - the gap between the duties society expects auditors to perform and those it is reasonable to expect of auditors. this component comprises the duties that society unreasonably expects auditors to perform. second, The performance gap - the gap between the duties society reasonably expects of auditors and what it perceives auditors actually accomplish. This component may be subdivided into: a- the deficient standards gap - the gap between the duties reasonably expected of auditors and auditors' existing duties as defined by the law, auditing standards, other regulations and professional promulgations; b- the deficient performance gap - the gap between the standard of performance of auditors' existing duties expected by society and auditors' performance of those duties as perceived by society.

-

مرحبا , الحقيقة هي أول مشاكة إلي بالمنتدى و طالبة نصيحة أهل المعرفة أنا خريجة محاسبة و عم ساوي master in auditing بالجامعة , و بصراحة أنا صحلي أنو إشتغل بمصرف خاص هون بالشام , و كمان عندي فرصة أنو اشتغل بمكتب deloitee بالشام أنا محتارة بصراحة و مترددة :confused:وين ممكن بلش حياتي المهنية , يعني الفرصتين كتير مناح و rewarding لذلك قررت أعمل بالمتل و اسئل مجرب , نصحوني

-

Labor acquisition event //.......... an economic increment event in which employee labor is purchased; each instance covers some time period; often represented by a timecard document Labor operation //...... an economic decrement event that uses up the employee labor resource Labor type resource //...... a resource-type entity set that represents a list of the kinds of labor activities that can be performed in labor operations Lapping //.............. a method of stealing cash whereby an employee steals cash from a customer payment, delays posting a payment to the customer's account, and then uses funds from a subsequent customer payment to post to the first customer's account; the process continues with the employee continually stealing from subsequent customer payments to post as prior customer payments Left join //............. a combination of tables based on a common attribute that includes unmatched records from the first table in the join and does not include unmatched records from the second table in the join; a partial outer join Level zero DFD //............. a high level (just under context level) representation that depicts only the very high-level processes within an information system Linkage relationship //..... an association between two resources to represent the fact that one of the resources is composed of the other; in the conversion cycle this provides a means for identifying the materials a finished good is composed of and the types of labor that are needed to produce a finished good Load (high and low) //........... the percentage of data values for an attribute that are non-null; if most cells in a column have actual values, the load is high; if most cells in a column have null values, the load is low Logical access control //........... restricting unauthorized access to the programs and data in systems Logical level implementation compromise //............. an implementation compromise made when converting a conceptual model into database objects Logical model //............ in database design, a model into which the conceptual model is converted once the type of database software to be used has been chosen (e.g., relational or object-oriented); hardware independent and somewhat software independent (if relational is chosen as the database type, then any relational software may be chosen but object-oriented software may not) Logical operator //............ Boolean search terms used in queries to define which records are included in the query result (examples include AND, OR, and NOT) Machine operation //............ an economic decrement event that partially consumes a machine in the conversion cycle Margin //............. the difference between value and cost in Porter's generic value chain model Marketing and sales //.......... primary value activities in Porter's generic value chain; activities associated with providing a means by which customers can buy products or services and the means for inducing them to buy Marketing event //........... an activity such as a sales call, advertising campaign, or promotion intended to inform customers about products and/or services and persuade them to trigger the sales/collection process; an internally instigated instigation event Master reference check //............. verifies that an event/transaction record has a corresponding master record to be updated Materiality of risk //........... a function of the size of the potential loss, its impact on achieving the enterprise's objectives, and the likelihood of the loss Materialization of task as entity //........... a conceptual model level implementation compromise in which an activity that could be reengineered is established as an entity (base object) Mathematical operation //........... a calculation that manipulates data values Maximum participation cardinality //........... represents the maximum number of times each instance of an entity set may participate in a relationship; legal values are one and N (many) Minimum participation cardinality //............ represents the minimum number of times each instance of an entity set must participate in a relationship; legal values are zero (optional participation) and one (mandatory participation) Model //........... a representation intended to serve as a plan or blueprint for something to be created; an object that represents in detail another (usually larger and more complex) object; used in systems design to help control complexity Monitoring //.............. one of COSO's five interrelated components of an internal control system; the process of assessing the quality of internal control performance over time and taking corrective actions as needed Move ticket //............. a document typically used in the conversion cycle to indicate the actual use of raw materials (i.e., the materials issuance event) Mutual commitment event //............. an event that obligates an enterprise to participate in at least two future economic events, one that increments a resource and another that decrements a resource Name conflict //............. a form of entity conflict in which two different entities are assigned the same name or a single entity is assigned two different names Noncash related economic event //.............. an activity in which a resource other than cash is increased or decreased Null to zero (Nz) function (in Microsoft Access) //.............. a Microsoft Access procedure used in querying that treats null values as if they are zeros Null value //............ a blank cell in a database table; a cell into which no data has been entered Object //............ a thing that has a physical or conceptual existence One-fact, one-place rule //........... a principle in database design that prohibits a pairing of a candidate key value with another attribute value from appearing multiple places in a database table and also prohibits multiple pairings of candidate key values with other attribute values in the same place; helps to ensure well-behaved relational tables Open purchase order file //............. a repository that contains information about purchase order events that have not yet been fulfilled by purchase events; a collection of unfilled purchase orders Open purchase requisition //............ a purchase requisition that has not yet been fulfilled by a purchase order Open sales invoice file //.......... a repository that contains information about sales events that do not yet have related cash receipts Open sales order file //............ a repository that contains information about sale order events that have not yet been fulfilled by sale events; a collection of unfilled sale orders Operating event //............. an activity performed within a business process to achieve enterprise objectives that does more than just communicate information (e.g., economic events, commitment events, and some instigation events) Operations //............ primary value activities in Porter's generic value chain; activities associated with transforming inputs into final products or services Operations list //.............. a document that identifies the labor types needed to create a finished good; captures the same information as the linkage relationship between labor types and finished goods Opportunity //............ a potential for reward Outbound logistics //........... primary value activities in Porter's generic value chain; activities associated with collecting, storing, and physically distributing products or services Outer join //............ a combination of tables based on a common attribute that includes unmatched records from both sides; accomplishes a set union of the tables Outflow //.............. the flowing out (disbursement or distribution) of a resource from an enterprise Packing slip //.......... a document that identifies the goods that have been shipped to a customer Parameter query (in Microsoft Access) //............ a query in which variables are used in lieu of data values as part of the query's selection criteria; allows the user to specify the data value to be used each time the query is run, thereby allowing reuse of the same query many times for different decisions Participation cardinalities //............ represents business rules for how many times an instance of an entity set is allowed to participate in a relationship Participation relationship //............. an association between an event and an internal or external agent Password //............. a unique identifier that only an authorized user of a system or application should know and that the user is required to enter each time he or she logs onto the system; a weak form of protection; a logical access control Pattern //........... a template or configuration from existing scenarios that can be used to make sense of other scenarios Paycheck //............. a document representing a cash disbursement (economic decrement event) to an employee Payroll clerk //.............. an internal agent responsible for accomplishing the cash disbursement event in the payroll transaction cycle Performance review //............ a review of some element of an enterprise's performance that provides a means for monitoring (e.g., comparison of actual data to budgeted or prior period data; comparison of operating data to financial data; and comparison of data within and across various units, subdivisions, or functional areas of the enterprise) Personal identification number (PIN) //.......... a numeric identifier used as a logical access control to authenticate a user; similar to a password Physical database model //............ a working database system that is dependent on the hardware, software, and type of software chosen during the design stages Physical level compromise //............... an implementation compromise made when entering the logical database objects into a database software package to create the working database Picking slip //............ a document that identifies the goods that have been taken out of the warehouse and made available to be shipped Posted key //............ an attribute of a database table that is added to another database table to create a link between the tables Preventive control //........... a control activity that focuses on preventing errors or irregularities either from occurring or from being entered into the enterprise information system Primary key attribute //........... a characteristic that uniquely and universally identifies each instance in an entity or relationship set Primary value activities //............. the events that create customer value and provide organization distinctiveness in the marketplace; events viewed as the critical activities in running a business Primitive DFD //............ the lowest level (most detailed) representation of a system process; cannot be further decomposed Primitive level data //............ data that cannot be decomposed into any component parts Procurement //.......... a support value activity in Porter's generic value chain; the function of purchasing inputs to a firm's value chain Production employee //........... an internal agent involved in labor operations and production runs in the conversion process; a worker who participates in the manufacture of finished goods Production order document //............ a document that captures information about a production order event Production order event //............ an event that represents the enterprise's commitment to engage in a future economic increment event (a production run) that will increase the finished goods resource Production run //........... an economic increment event that increases the quantity of a finished goods resource Production supervisor //.......... an internal agent who authorizes events in the conversion cycle Project //......... a relational algebra operator (pronounced pro-JECT' rather than PRO'-ject) that specifies a vertical subset to be included in the query result Proposition relationship // ........ an association between an instigation event and a resource or resource type; often specifies quantity and proposed cost or selling price for the item(s) identified as needed Purchase //........ an economic increment event in which services or the title to goods transfers from a supplier to the enterprise; also called an acquisition Purchase order //......... a mutual commitment event in which a supplier agrees to transfer title of goods to the enterprise at an agreed upon future time and price and the enterprise agrees to pay for those goods; a document reflecting the terms of the mutual commitment event Purchase requisition //......... an instigation event in which the need for goods or services is identified; an internal document that communicates this need to the enterprise purchasing function Purchase return //......... an economic increment reversal event in which the title to goods previously transferred from a supplier to the enterprise is transferred back to the supplier Query //....... a request for information submitted to a database engine Query by example (QBE) //...... a type of query interface intended to be more "point and click" in nature than is SQL; in this interface the user creates a visual example of what tables and fields should be included in a query result and specifies any calculations to be included Query grid (in Microsoft Access) //........ the lower half of the QBE view into which fields are dragged and in which aggregations or horizontal calculations may be created to establish the desired logic for a query Query window (in Microsoft Access) //....... the screen in which queries are created; user may toggle back and forth between QBE design, SQL design, and Datasheet (result) views within the query window Range check //........ an instruction in a computer program that compares entered data to a predetermined acceptable upper and/or lower limit and rejects data that falls outside the specified limits unless special authorization is obtained Raw material //....... an input resource in the conversion process that is completely used up in the transformation to finished goods Raw material issuance //........ an economic decrement event involving the using up of raw materials in the production process; the raw materials are usually transformed into finished goods and lose their own identity and nature in the process Raw material requisition //....... a commitment event whereby the inventory clerk or warehouse supervisor commits to the production supervisor to transfer materials from the materials warehouse to the production floor; assumes the raw materials are available within the enterprise and reserves them for use REA core pattern //........ the original version of the REA model at the business process level; includes resources, economic events and agents, duality relationships, stockflow relationships, and control (participation) relationships Read-only file designation //......... a property used to mark data as available for reading only; the data cannot be altered by instructions from users, nor can new data be stored on the device Reality //........ that which exists objectively and in fact REA ontology //........ a domain ontology founded by Bill McCarthy at Michigan State University that attempts to define constructs that are common to all enterprises and demonstrate how those constructs may be represented in an integrated enterprise information system. The REA ontology is made up of four layers: the value system, value chain, business process, and task levels. Reasonableness check //....... an instruction in a computer program to verify whether the amount of an event/ transaction record appears reasonable when compared to other elements associated with each item being processed Receiving report //...... a document that lists the items and the quantities and condition of each item received in an acquisition event; the receiving report identifier is often used as the identifier for the acquisition event Reciprocal relationship //....... a relationship between a commitment to an economic increment and a commitment to an economic decrement; the commitment level equivalent of the duality relationship; in the conversion cycle, represents a schedule of what is to be produced and what will need to be used and consumed in the production process Record //....... a row in a relational database table Redundancy //......... in database design, duplicate storage of the same information Reengineering //........ the redesign of business processes or systems to achieve a dramatic improvement in enterprise performance Referential integrity // ........ a principle in relational databases that requires a value for a foreign key attribute to either be null (blank) or to match exactly a data value in the table in which the attribute is a primary key Relational algebra // ...... the original data manipulation (querying) language that was constructed based on set theory and predicate logic as part of the relational database model; primary operators include Select, Project, and Join; however, other operators are also part of the relational algebra Relational database //....... a collection of tables that meet the criteria of the relational model Relational model //......... a logical level database design model developed by E. F. Codd based on set theory and predicate logic; primary constructs are relations (tables) that represent entities and relationships between entities Relational table //......... a relation; a two-dimensional storage structure (i.e., a storage structure with rows and columns) that represents either an entity or a relationship between entities and that adheres to relational principles such as entity integrity, referential integrity, and the one-fact, one-place rule Relationship //............ an association between two or more entity sets Relationship conflict // ........ a discrepancy in the assignment of participation cardinalities or in the label used to name the same relationship in different view models Relationship layout (in Microsoft Access) //........ a window in which relationships between tables are visually depicted Remittance advice //........ a document (usually the portion of a customer invoice or statement that says "return this stub with payment") that advises the enterprise the customer is remitting payment; often used as the identifier for a cash receipt event Rental // .......... an economic decrement event that does not involve the transfer of title of goods, but instead involves a transfer of the right to use goods for an agreed upon length of time; begins when the right to temporary possession of the goods transfers from the lessor to the lessee and ends when possession of the goods transfers back from the lessee to the lessor Repeating group //......... multiple facts stored in one place; the same value of a key attribute field associated with multiple values of another attribute Representation //.......... a surrogate for something; a symbol that closely resembles the actual construct; the closer the resemblance to the real object, the better the representation Request to return goods //......... notification to a supplier of the enterprise's dissatisfaction with goods that seeks permission to return those goods in lieu of making payment (or in exchange for a refund) Required data entry (field property) (in Microsoft Access) //........... a choice specified in table design view; a user will not be allowed to enter a record into the table without including a value for any field(s) for which this property is set to "yes"; a user may leave any field except the primary key field(s) blank for which this property is not set to "yes" (Microsoft Access automatically enforces entity integrity so there is no need to set the required data entry field property to "yes" for primary key fields) Reservation relationship //......... an association between a mutual commitment event and a resource or resource type; often specifies quantity and budgeted cost or selling price for the item(s) involved in the agreement Resource // ......... a thing of economic value (with or without physical substance) that is provided or consumed by an enterprise's activities and operations Resource flow // ......... the increase or decrease of a resource as the result of an event Resource inflow //........ the increase of a resource as the result of an event Resource outflow //......... the decrease of a resource as the result of an event Reversal relationship //.......... an association between an economic reversal event and a resource or resource type; often specifies the quantity and cost or selling price information for the item(s) involved in the event Right join //....... a combination of tables based on a common attribute that includes unmatched records from the second table in the join and does not include unmatched records from the first table in the join; a partial outer join Risk // ........... an exposure to the chance of injury or loss Risk assessment //......... one of COSO's five interrelated components of an internal control system; the identification and analysis of relevant risks associated with the enterprise achieving its objectives; forms the basis for determining what risks need to be controlled and the controls required to manage them Row //.......... the data attribute values that apply to a single instance of an entity or relationship set as represented in a relational database table Sales/collection process //......... transaction cycle in which goods or services are exchanged to customers or clients for cash or some other form of compensation Sales call //........... An internally initiated instigation event; typically involves a sales representative calling on a customer, either via telephone or in person, to describe the features of one or more products or services Sales invoice // ........... a document used to communicate to a customer the fact that the enterprise has fulfilled a commitment to transfer title of goods to the customer; sometimes also serves as a request or reminder for the customer to fulfill its commitment and remit payment to the enterprise Sales order //........... a mutual commitment event in which the enterprise agrees to transfer title of goods to a customer at an agreed upon future time and price and the customer agrees to pay for those goods; a document reflecting the terms of the mutual commitment event Sales return //......... an economic decrement reversal event in which the title to goods previously transferred to a customer transfers back to the enterprise Schedule //......... a mutual commitment event in the human resource business process wherein the employee agrees to provide labor as specified in the schedule and the enterprise commits to pay the employee the contracted wage rate for the labor provided Schema //........... the column headings, or intension, of a relational database table Script //.......... a sequence of events that typically occur in combination with each other Select //........... a relational algebra operator that specifies a horizontal subset to be included in the query result Select-From-Where //........... the format of SQL queries; the Select clause specifies a vertical subset to be included in the query result; the From clause specifies which table(s) are to be queried and any subgrouping to be done; the Where clause specifies a horizontal subset to be included in the query result and, if multiple tables are included, helps to define the join Semantic orientation //.......... a goal of REA-based systems that requires objects in the system's conceptual model to correspond as closely as possible to objects in the underlying reality Separation (or segregation) of duties //......... the structuring of employees' job functions such that one employee is prohibited from performing two or more of the following functions: authorization of transactions involving assets, custody of assets, record keeping, and reconciliation; reduces the opportunity for one employee to steal enterprise assets and to conceal the theft in the normal course of his or her work Sequence check //....... a control used to verify the records in a batch are sorted in the proper sequence and/or to highlight missing batch items Service //.......... primary value activities in Porter's generic value chain; activities associated with providing service to enhance or maintain the value of the products or services Service engagement //........ an economic decrement event in which the enterprise transfers services to a customer Service type // ......... a kind of service an enterprise has the ability to provide to customers; a resource type Shares of stock // ....... units that represent the holder's right to share in various ownership interests of an enterprise Show Table window (in Microsoft Access) //......... a screen from which the user may choose which table(s) to include in the relationship layout or in a query Simple attribute //......... a characteristic of an entity or relationship that cannot be further decomposed into component characteristics Smart card or token //.......... a logical access control that authenticates a user through a hardware device combined with a log-in password process; the smart card generates a random code that changes at predetermined intervals and must be matched against the host system; the user must also enter a password to gain access to the system SQL view (in Microsoft Access) //....... a mode for viewing the underlying SQL statement for a query; even if a query was created in QBE mode, Microsoft Access generates a corresponding SQL statement that the user may view to evaluate the query's logic Statement on Auditing Standards No. 94 //........ an auditing statement that largely established current standards for internal control Static derivable attribute //....... a derivable attribute for which the derived value will not change if additional transaction data is entered into the database Stockflow relationship //...... an association between an economic event and a resource or an association between an economic reversal event and a resource; often specifies quantity and actual cost or selling price for the item(s) involved in the event Stock issuance commitment event //..... an equity financing agreement that commits an investor to provide a determinable cash dollar amount (stock proceeds) on a specified date Stovepipes //..... functional areas structured such that the only pathways for communication are at the top (i.e., between the managers of each area); also called functional silos Strategy //....... an enterprise's planned course of action for achieving an objective Structured Query Language (SQL) //......... a query language developed to enable the performance of multiple operations in a single query and to use a standard format for every query statement (Select-From-Where) to simplify the task of query development Structuring orientation //.......... a goal of REA-based systems that demands the use of a pattern as a foundation for the enterprise system to facilitate automated reasoning by intelligent software interfaces to the enterprise system Sum //......... the mathematical total of a column of numerical data values Supplier //........ a person or organization from which an enterprise purchases goods or services Supply chain // ....... the entire network of enterprises (e.g., retailers, wholesalers, transportation firms) involved in providing a particular product or service to an end customer Support value activities //......... in Porter's generic value chain, activities that facilitate accomplishing the primary value activities Symbol //.......... something that stands for or represents something else Synonym //....... a word that has the same meaning as one or more other words Syntax //....... the formatting rules of a query language (and also other types of languages) System flowchart //........ a graphical representation of the inputs, processes, and outputs of an enterprise information system; includes details about the physical as well as the logical aspects of the system components Task level REA model // ...... a task is a workflow step or activity that may be changed or eliminated without fundamentally changing the nature of the enterprise and therefore should not serve as a foundational element in an enterprise information system; task level models in the REA ontology are graphical representations of workflow processes for which there is no identified pattern Technology development //......... support value activities in Porter's generic value chain; the know-how, procedures, or technology embedded in processes that are intended to improve the product, service, and/or process Threat //...... a situation or event that causes possible or probable loss to a person or enterprise Timecard //......... the primary document prepared by the enterprise in conjunction with the economic increment event; may be completed on a daily, weekly, or other basis; is typically completed by employees and approved by supervisors; lists the times employees started working (punched in) and stopped working (punched out) for each day in the covered time period Token //.......... an individual object; token-level representation uses a separate token for each individual instance in the piece of reality that is being modeled Training //...... the provision of education to employees to further develop their skills and/or knowledge Transfer duality relationship //...... an association between economic increment and decrement events in which the resource(s) decremented are traded for the incremented resource(s) Transformation duality relationship // .......... an association between economic increment and decrement events whereby the resource(s) decremented are changed into the incremented resource(s), i.e., the incremented resource(s) is created from the decremented resource(s) Tuple //....... a row in a relational database table Type // ......... a category into which individual objects may be classified; type level representation uses one type to represent as many individual instances as fit the category Typification //....... a relationship between an entity and an entity type; allows for storage of characteristics of entity categories Use stockflow relationship //........... a relationship between a resource and an economic decrement event whereby the resource is completely subsumed by the decrement (i.e., the resource is completely used up) Validity check //........ an internal control in which a comparison is made between entered data and prespecified stored data to determine whether the entered data is valid Valid sign check //....... an internal control used to assess whether a field's sign (positive or negative) makes sense; used to highlight illogical values, particularly balances in master file records Value chain //........ the interconnection of business processes via resources that flow between them, with value being added to the resources as they flow from one process to the next Value chain level REA model // a representation that depicts the interconnected business processes for an enterprise, the resource flows between the processes, and the duality relationships within each process Value system //....... an enterprise placed into the context of its various external business partners such as suppliers, customers, creditors/investors, and employees Value system level REA model // a representation that depicts the resource exchanges in which an enterprise engages with external business partners Vendor invoice //......... a document sent by a supplier to the enterprise to communicate the fact that the supplier has fulfilled its commitment to transfer title of goods to the enterprise; sometimes also serves as a request or reminder for the enterprise to fulfill its commitment and remit payment Vertical calculation //....... a computation that is a summarization of data values within a single column; also called an aggregation function Vertical subset of a table //........ a part of a table that includes only some of the table's columns (but includes all the rows) View integration //....... the process of combining separate conceptual models into one comprehensive model View modeling //.......... the creation of conceptual models to represent separate parts (usually transaction cycles) of an enterprise Virtual close //....... the ability to produce financial statements without actually closing the books; often touted as a benefit of ERP system software Voice recognition technology //........ used for internal control, creates a digital representation of a person's voice and stores it in a database; to access a resource the person speaks into a device; the spoken voiceprint is compared to the stored voiceprint and the person is denied access if the voiceprints do not match Volatile derivable attribute //..... a derivable attribute for which the derived value will change if additional transaction data is entered into the database Withholdings // .... employee pay amounts retained by the employer to remit to governmental or other agencies on behalf of the employee (e.g., social security, income tax, health insurance premiums) Workflow //......... detailed procedural steps and activities used to accomplish events and business processes in enterprises XBRL //..... Extensible Business Reporting Language; a tagging language used to identify data values of business reporting line items such as financial statement elements XML //..... Extensible Markup Language; a tagging language used in the creation of websites .

-

السلام عليكم و رحمة الله و بركاته الحمد لله و الصلاة و السلام على رسول الله أعتذر عن الغياب و أعود للمشاركة بمشيئة الله هذا لكتاب يبدوا جيد و قرأت فيه و أرجو من المهتمين إعطاء تعليقهم عليه و أعود لمتابعة كافة موضوعاتي المعلقة بمشيئة الله كذلك أرفع من مكتبتي ما أجده ملائما و ما أحلى العودة للبيت أخوكم حسن JW Integrated Auditing of ERP Systems.pdf

السلام عليكم و رحمة الله و بركاته الحمد لله و الصلاة و السلام على رسول الله أعتذر عن الغياب و أعود للمشاركة بمشيئة الله هذا لكتاب يبدوا جيد و قرأت فيه و أرجو من المهتمين إعطاء تعليقهم عليه و أعود لمتابعة كافة موضوعاتي المعلقة بمشيئة الله كذلك أرفع من مكتبتي ما أجده ملائما و ما أحلى العودة للبيت أخوكم حسن JW Integrated Auditing of ERP Systems.pdf -

دورات عاليه المستوى ولمبتدئين وللمديرين اتصل على 0020166293935 0020502573737 Mohwaghjas@yahoo accounting(eng-arabic)peachtreequickbooksoffice accountingexcel-accesspayrollexcel analysis-pivotbudgetingfinansial analysis tools and techniques for managersaccounts payablereceivableswriting business lettres inventorymsprojectfinancial management and analysisinternational auditingexcel data analysis

-

انظر البحث المرفق استكمال بناء المعايير الوطنية والعربية للمحاسبة في ضوء المعايير الاسلامية: دراسة مقارنة لدول السعودية ومصر وماليزيا ومجلس التعاون لدول الخليج العربية د . محمد شريف توفيق أستاذ المحاسبة المالية كلية التجارة – جامعة الزقازيق http://www.mstawfik.bizhosting.com sherif_tawfik@yahoo.com ملخص البحث Abstract : بالاطلاع علي تجارب الدول العربية في بناء معاييرها للمحاسبة نجد ان معظمها يتميز بخصائص: البعد عن اصدار معايير اسلامية للمحاسبة – عدم وجود تنظيم متكامل لاصدارها ومتابعتها بكل جديد – عدم وجود موقع مستقل علي الانترنت لمتابعتها وغير ذلك. وعلي خلاف ذلك لاحظ الباحث تميز التجربة الماليزية وشمولها لاهم المعايير الاسلامية. كذلك تصدر هيئة المحاسبة والمراجعة للمؤسسات المالية الاسلامية AAOIFI بالبحرين معايير محاسبية طبقا للشريعة الاسلامية لم يتم الاستفادة منها بعد بالكامل. وقد دفعت تلك الاعتبارات الباحث لبحث موضوع بيان سبل استكمال بناء تلك المعايير الوطنية والعربية. وقد تناول البحث هذه الاعتبارات من خلال قسمين: الاول شمل دراسة مقارنة لخصائص بناء المعايير في الدول والهيئات الوطنية والعربية، وعرض وتقييم التجارب المصرية والماليزية والسعودية ومجلس التعاون الخليجي في بناء معايير المحاسبة المالية. اما القسم الثاني فشمل اطارا مقترحا لبناء المعايير الاسلامية لمحاسبة الزكاة السعودي وعرض القوائم المالية في المؤسسات المالية الاسلامية من المعيار الماليزي. وقد انتهي البحث الي بيان مدي شمول وجودة التجربة الماليرية واوجة قصور واستكمال التجارب العربية في بناء المعايير المحاسبية من خلال: ضرورة استكمال محورها التنظيمي وانشاء مجالس معايير المحاسبة ومواقعها علي الانترنت وبناء معاييرها الاسلامية ودعمها بكل جديد. ويتعين قي هذا الشأن الاسترشاد بتجربة الـ 21 معيار اسلامي Shari’a Standards (SSs) التي اصدرتها هيئة المحاسبة والمراجعة للمؤسسات المالية الاسلامية Accounting and Auditing Organization for Islamic Financial Institutions عام 2005 بمملكة البحرين. is.pdf

-

ارفع لكم مقاله رائعه للاستاذ الدكتور الرائع ........احمد ابو موسى تتعلق بتدقيق الاعمال الالكترونية .......... ادعو لنا Auditing E-business.pdf

-

ملخص البحث Abstract : بالاطلاع علي تجارب الدول العربية في بناء معاييرها للمحاسبة نجد ان معظمها يتميز بخصائص: البعد عن اصدار معايير اسلامية للمحاسبة – عدم وجود تنظيم متكامل لاصدارها ومتابعتها بكل جديد – عدم وجود موقع مستقل علي الانترنت لمتابعتها وغير ذلك. وعلي خلاف ذلك لاحظ الباحث تميز التجربة الماليزية وشمولها لاهم المعايير الاسلامية. كذلك تصدر هيئة المحاسبة والمراجعة للمؤسسات المالية الاسلامية AAOIFI بالبحرين معايير محاسبية طبقا للشريعة الاسلامية لم يتم الاستفادة منها بعد بالكامل. وقد دفعت تلك الاعتبارات الباحث لبحث موضوع بيان سبل استكمال بناء تلك المعايير الوطنية والعربية. وقد تناول البحث هذه الاعتبارات من خلال قسمين: الاول شمل دراسة مقارنة لخصائص بناء المعايير في الدول والهيئات الوطنية والعربية، وعرض وتقييم التجارب المصرية والماليزية والسعودية ومجلس التعاون الخليجي في بناء معايير المحاسبة المالية. اما القسم الثاني فشمل اطارا مقترحا لبناء المعايير الاسلامية لمحاسبة الزكاة السعودي وعرض القوائم المالية في المؤسسات المالية الاسلامية من المعيار الماليزي. وقد انتهي البحث الي بيان مدي شمول وجودة التجربة الماليرية واوجة قصور واستكمال التجارب العربية في بناء المعايير المحاسبية من خلال: ضرورة استكمال محورها التنظيمي وانشاء مجالس معايير المحاسبة ومواقعها علي الانترنت وبناء معاييرها الاسلامية ودعمها بكل جديد. ويتعين قي هذا الشأن الاسترشاد بتجربة الـ 21 معيار اسلامي Shari’a Standards (SSs) التي اصدرتها هيئة المحاسبة والمراجعة للمؤسسات المالية الاسلامية Accounting and Auditing Organization for Islamic Financial Institutions عام 2005 بمملكة البحرين. http://mstawfik.tripod.com/is.pdf

-

السلام عليكم و رحمة الله و بركاته يمكنكم الان الاطلاع على مجموعة رائعة من المراجع الانجليزية، في جميع مجالات المعرفة و كل المواضيع التي تهمكم، وخاصة corporate governance,auditing, ....و غيرها من المواضيع و ذلك من خلال الرابط التالي:http://eu.wiley.com/WileyCDA